California Health Care

Health Care Sharing Ministry (HCSM) plans are a way for people with similar faiths and beliefs to pool their money, helping members cover their medical expenses. These plans are not insurance, and membership in these nonprofit groups comes with both advantages and disadvantages.

Learn the basics of health sharing plans, including the types you may encounter, their advantages and disadvantages and when a HCSM plan may be the right choice for you.

What Are Health Sharing Plans?

Traditional insurance plans, provided by companies or government programs, offer guaranteed payments under predefined conditions. Health share plans, on the other hand, are healthcare funding co-ops. These programs are typically faith-based, with members who share a common set of practices and beliefs.

They are commonly referred to as medishare plans or health sharing ministries. HCSM’s are nonprofits that serve as alternatives or additions to traditional insurance. Members’ monthly contributions create a pool the...

A preventive care eye exam is essential for maintaining optimal eye health and vision clarity. During this comprehensive evaluation, eye care professionals assess your vision and overall eye health. This examination can detect early signs of eye diseases and systemic conditions, making regular checkups vital.

This article explores what to expect during a preventive care eye exam, including the tests performed, their importance and how they contribute to your overall well-being.

Eye care professionals, such as optometrists or ophthalmologists, conduct preventive eye examinations as part of routine health care. They assess eye health and identify potential problems or diseases before they escalate. The procedure and type of examinations differ based on the situation but often include the following components:

Based on the results, the eye care professional will recommend treatments or corrective measures and may advise on follow-up care. They may also provide prescriptions for glasses or c...

Accessing free services through health insurance can promote wellness and prevent illness. In California, health insurance plans often cover various services at no additional cost. These services improve individual health outcomes and contribute to overall community well-being. Understanding and utilizing these free benefits can empower Californians to take charge of their health and access the care they need for a healthier life.

Health insurance provides financial protection and access to care. There are different types, including individual and employer-sponsored plans. Employers provide employer-sponsored coverage to their employees as part of their benefits package. Individuals or families can also purchase plans directly from insurance companies or the insurance marketplace. Covered California is the state’s health insurance marketplace.

California residents can access diverse health insurance plans through Covered California, including Medi-Cal and Medicare. Medi-Cal is the sta...

A secondary dental insurance plan means two dental insurance plans cover you at once. If two dental insurance plans cover you, you have dual dental coverage or supplemental dental insurance.

This article explains how it’s possible to have coverage from a second dental plan, how it works and how it can benefit you.

It is possible to have coverage from two dental insurance plans at once. This is called dual coverage or supplemental insurance, and it usually happens in one of three situations:

When you have a secondary dental plan, your two plans will have terms that specify how the coordination of benefits (COB) between them will work. State regulations can also impact COB. Therefore, you must check your policy documents or contact your insurers to clarify the specifics.

However, you will find that one of your coordinating plans is designated as your primary plan and the other as secondary insurance:

If your plans are with two different companies and you claim from both, the secondary car...

You can get health insurance without a Social Security number (SSN). If you or a family member doesn’t have an SSN for several reasons, yet you need health insurance, you may wonder if the lack of an SSN would be an obstacle. While you can still get health insurance, you’ll need to meet several conditions to get health insurance without an SSN.

The health insurance marketplace requires an applicant’s SSN to confirm their legal presence in the United States and confirm their projected income matches the information from trusted sources, including Equifax Workforce Solutions, the Social Security Administration and the IRS.

You can still apply for health coverage if you don’t have an SSN if you’re lawfully present in the United States and one of the following is true:

To be eligible to use the U.S. health coverage marketplace, you must:

If you’ve confirmed you can apply for and get health insurance, you may still wonder whether you can add your undocumented family members to yo...

Almost all insurance providers implement lock-in periods — a time period where insurance users cannot change or cancel their policy. Also known as a waiting period, lock-in periods are designed to protect an insurance company’s interests and keep policyholders from misusing plans for short-term coverage.

As someone who needs insurance, understanding terms like lock-in periods is crucial in avoiding surprises and penalties. Learn more about how they can affect you with Health for California.

Lock-in periods almost exclusively benefit an insurance company. Most businesses implement them to:

The most common types of lock-in insurance you’ll see are:

If insurance companies benefit from lock-in insurance periods, does that mean it can’t benefit you? Not necessarily. If you go into your policy understanding how a lock-in period will affect you, you can do everything in your power to avoid situations where you’ll incur penalties. Still, the implications remain that:

Lock-in periods in in...

As you get older and look forward to the day when you can quit the daily grind, it’s important to consider the practical aspects of retirement. If you think it’s time to retire, your age can impact your retirement benefits, such as Social Security and when you can qualify for Medicare.

Here are some frequently asked questions about the full retirement age and how it may impact your retirement planning.

Full retirement age, also called FRA or normal retirement age, is the age you must reach to collect full, unreduced Social Security retirement benefits.

In 2024, the normal retirement age for anyone born in 1960 or later was 67. Check out the Social Security Administration’s (SSA) Retirement Age Calculator to learn your full retirement age.

Social Security benefits are based on how much you earned during your working career. If you choose to start receiving benefits at 65 and you worked steadily, you may have higher lifetime earnings than someone who did not work throughout their ad...

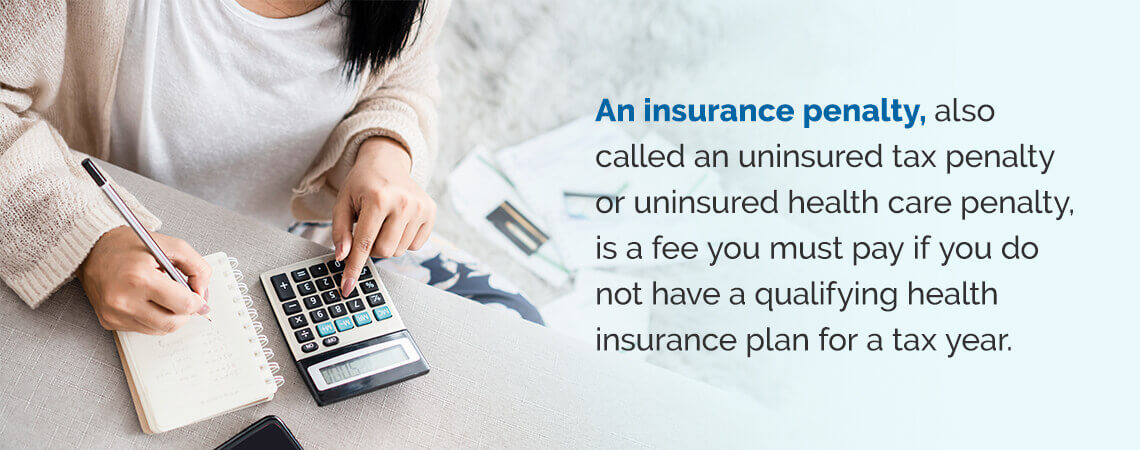

The California state government requires residents to have health insurance, or they may face a tax penalty. The options are either enrolling in a qualified health insurance plan or paying the tax penalty, subject to some exceptions. Having health insurance is the better option since it provides many benefits.

It’s a good idea to understand the tax implications of not having health insurance. Health for California helps Californians get the health coverage that’s right for them.

There is a tax penalty for not having health insurance in California. The insurance penalty, also called the uninsured health care penalty or uninsured tax penalty, is a fee you must pay if you do not have a qualifying health insurance plan for a tax year. These penalties used to be in place at a federal level with the Affordable Care Act, popularly known as Obamacare, in 2014. They required most legal residents or United States citizens to purchase qualifying health insurance or pay a tax penalty.

The...

by Wendy Barnett

When you have lost your job, your medical insurance from your employer can end, too. Being without work can be a stressful time, but understanding your health insurance options doesn’t have to be. Explore your options for health insurance after losing your job with Health for California.

From the day you lost your job and health insurance coverage, you have 60 days to apply for health insurance, regardless of what time of year it is.

Since the Affordable Care Act went into law, most health insurance enrollment is limited to the Open Enrollment period at the end and beginning of every year. When Open Enrollment is closed, you typically have to wait for the next enrollment period to apply for coverage. However, this time is also known as the Special Enrollment Period, meaning you can find coverage if you experience a Qualifying Life Event. Involuntarily losing your job is considered one of these Qualifying Life Events.

It’s also important to know that searching for...

If you are a California resident needing health care coverage, it can be challenging to untangle terms like Medi-Cal, Medicaid and Medicare. This guide will help you understand Kaiser Medi-Cal as a solution to cover your medical needs, how it relates to Medicaid and Medicare and how you can apply for coverage.

Medi-Cal is the same as Medicaid in California. It is a federal and state-supported form of insurance that pays for various medical services for California residents with limited income and resources. While Medicaid is the larger nationwide program, Medi-Cal is California’s Medicaid. Each state sets its own eligibility criteria and benefits, so it is important to consult sources specific to Medi-Cal for accurate information about Medicaid in California.

Kaiser Permanente is the oldest and largest Health Maintenance Organization (HMO) in the United States. Its largest membership is in California. If you qualify for Medi-Cal, you can choose Kaiser’s Medi-Cal plan as your he...